Confusion between life insurance and death insurance is common. However, they are two very different types of contracts. What characterizes these contracts?

How and for what purpose can you take them out? Explanation.

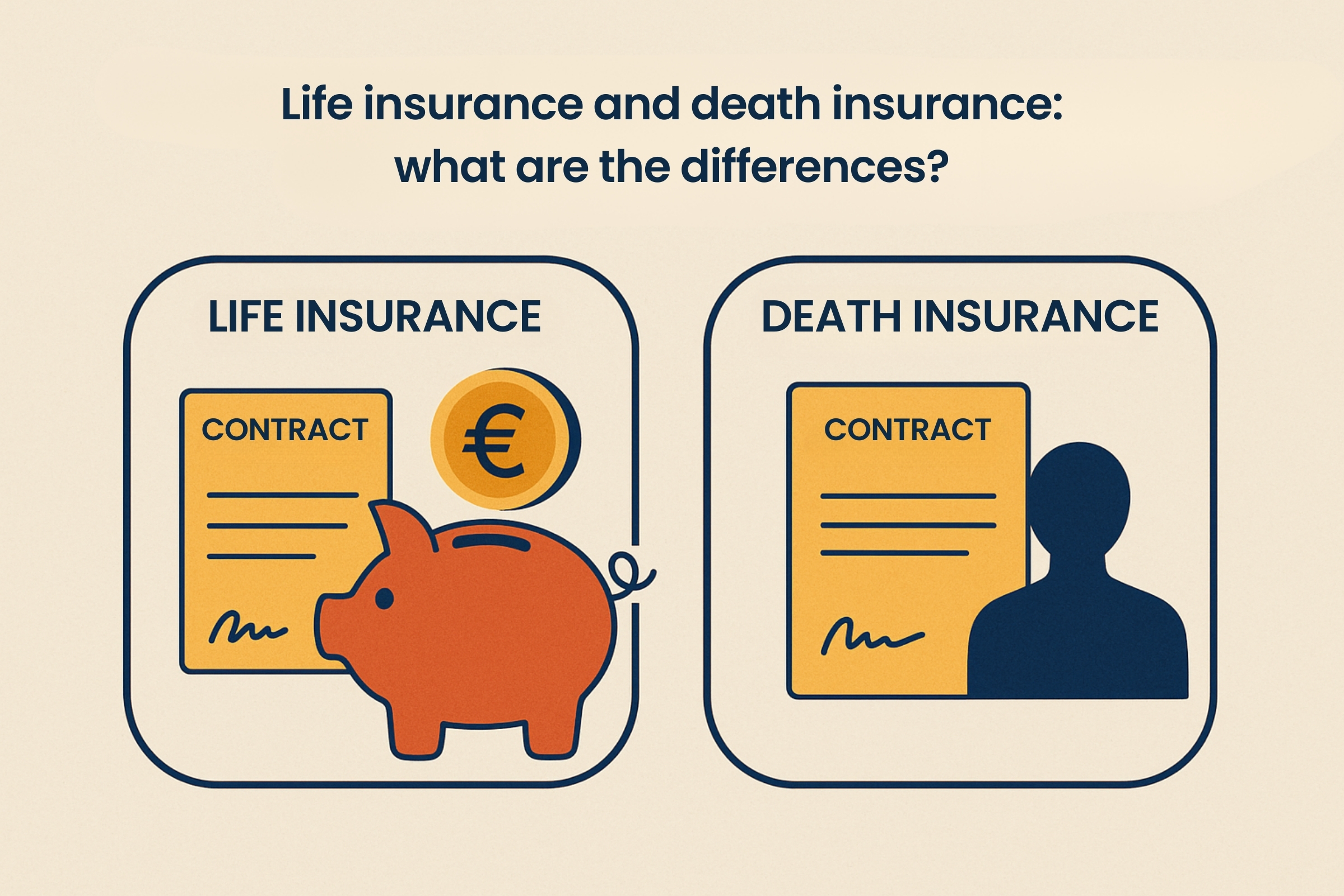

Life Insurance: What Are Its Features?

Life insurance is a medium- to long-term savings product.

Once the contract is opened with an initial deposit, you can make contributions (also called premiums), regular or not, without any limit on the amount.

When the contract ends, the beneficiaries (yourself or a third party designated in the contract) receive the accumulated capital or a lifetime annuity.

Life insurance is also an interesting investment tool for estate planning. It allows you to designate one or more beneficiaries through the beneficiary clause.

Contracts taken out in the name of a spouse, civil union partner (PACS), certain non-profit organizations, or in favor of siblings, may under certain conditions be exempt from inheritance tax.

In other cases, the capital may be taxable depending on:

- the date the contract was opened,

- the date of payments,

- your age at the time of payments,

- the amount of capital paid to beneficiaries.

What Are the Main Types of Life Insurance Contracts?

When you take out life insurance, you can choose between two main types of contracts:

- Single-asset contracts, also called euro funds,

- Multi-asset contracts, also called unit-linked contracts.

Contributions made to a euro fund are guaranteed, but the return is limited.

Multi-asset contracts usually include a portion in euro funds and a portion in unit-linked investments. Unit-linked life insurance is riskier than euro funds.

Important: there is no guarantee you will get back your full investment if you choose unit-linked funds.

You may suffer capital losses depending on financial market fluctuations. That’s why it’s recommended to invest over the long term to smooth out market volatility and maximize potential returns.

Investing in unit-linked funds gives you access to a wide range of financial instruments with varying degrees of volatility.

Thus, before investing in unit-linked funds, it’s important to determine your risk profile with your bank advisor or insurance company, your wealth goals, and your investment horizon.

Unit-linked funds are typically invested in shares of mutual funds (UCITS) that hold stocks or bonds. Your payments can also be invested in property funds through real estate investment companies (SCPI).

Life Insurance: A Flexible Investment

Life insurance is notable for its flexibility.

When you take out a life insurance policy, you are free to request partial redemptions or a full withdrawal of your accumulated capital at any time.

This option is subject to the beneficiary’s acceptance (which may be a different person than the contract holder). The beneficiary must provide written consent if they have accepted their designation according to the legal procedure.

A full withdrawal terminates the contract. You can also ask your insurer for a loan (advance) on your contract. This advance is a loan granted by the insurance company, and interest is charged at the rate set in the contract.

What Are the Tax Rules for Life Insurance?

Life insurance is attractive in part due to its tax advantages. Only gains are taxable when you make a withdrawal (partial or full).

The taxation of life insurance depends on several factors:

- the date of premium payments,

- and the contract’s duration.

Since September 27, 2017, gains from premiums paid after that date are subject to a flat tax (PFU) of 30% if the contract is less than eight years old.

After eight years, you benefit from an annual tax exemption of €4,600 (or €9,200 for married or civil union couples filing jointly), and a reduced tax rate of 24.7% on gains (income tax and social contributions) if the total premiums paid are less than €150,000.

Tax on Gains from Premiums Paid Before September 27, 2017

For premiums paid before this date, your gains are subject to either:

- the progressive income tax scale via your tax return, or

- a withholding flat tax (PFL) if you choose it.

In all cases, social contributions of 17.2% also apply.

| Contract Age | Taxation |

| 0 to 4 years | Income tax scale or PFL at 35% + 17.2% social contributions |

| 4 to 8 years | Income tax scale or PFL at 15% + 17.2% social contributions |

| Over 8 years | Income tax scale or PFL at 7.5% + 17.2% social contributions |

Tax on Gains from Premiums Paid After September 27, 2017

For premiums paid after this date, gains are taxed based on the contract’s duration and the amount of premiums paid.

| Contract Age | Taxation |

| 0–8 years | Flat tax (PFU): 30% (= 12.8% income tax + 17.2% social contributions) |

| Over 8 years with premiums < €150,000 | 7.5% income tax + 17.2% social contributions |

| Over 8 years with premiums > €150,000 | PFU: 30% (12.8% + 17.2%) |

The €150,000 limit applies to all your life insurance contracts combined.

According to the tax authorities, when your total premiums across all contracts exceed €150,000, only the portion of gains related to the first €150,000 in premiums qualifies for the 7.5% rate.

If you wish, you can opt for taxation under the progressive income tax scale, but this will then apply to all your investment income.

Additional Notes:

Individuals whose reference taxable income (revenu fiscal de référence) in year N-2 is below €25,000 (or €50,000 for joint taxpayers) may request exemption from the non-liberatory withholding tax (12.8% or 7.5%).

After 8 years, you benefit from an annual exemption of €4,600 (€9,200 for married/PACS couples filing jointly) on your withdrawal gains — this portion is not subject to income tax.

In Which Cases Can You Be Exempt from Tax?

You may be exempt from income tax on withdrawals or contract termination if you are:

- dismissed from your job,

- liquidated due to bankruptcy,

- forced into early retirement,

- officially recognized as disabled (categories 2 or 3).

You must be the policyholder or their spouse/PACS partner, and the contract must be closed by the end of the year following the qualifying event.

Lifetime Annuity Payments: How Are They Taxed?

Life insurance allows you to convert your capital into a lifetime annuity. Your insurer guarantees periodic payments (monthly, quarterly, or semi-annually) until your death.

This option is irreversible: you permanently give up control over the capital in your contract. Therefore, you cannot pass on your life insurance at death.

The annuity amount depends on:

- the size of the capital,

- your age when the annuity begins.

The annuity is taxable (income tax and social contributions).

The taxable portion of the annuity depends on your age at first payment and is fixed as follows:

- 70% taxable if you are under 50,

- 50% if you are between 50 and 59,

- 40% if you are between 60 and 69,

- 30% if you are over 69.

Death Insurance: What Is It?

Death insurance is a protection policy. You pay premiums to the insurance company, which pays a lump sum or annuity to your beneficiaries upon your death.

Unlike life insurance, you cannot be the beneficiary yourself. You must designate one or more people as beneficiaries when signing the contract. The amount to be paid is also fixed at the time of signing.

There are two types:

- Term death insurance: valid for a set period,

- Whole-life death insurance: valid indefinitely.

Insurance to Protect Your Loved Ones

Death insurance is a tool to protect your family financially against unexpected life events, especially if you die or become permanently disabled.

Depending on the policy, additional coverage may include:

- Accidental death,

- Total and irreversible loss of autonomy,

- Illness (if diagnosed after the contract starts),

- Temporary unemployment.

How Much Does Death Insurance Cost?

The cost of death insurance varies by contract and the capital to be paid to beneficiaries.

The premium also depends on your personal situation:

- your age at contract start,

- your lifestyle,

- your health condition.

What Tax Applies to the Capital From Individual Death Insurance?

The capital paid to the designated beneficiaries is not part of the estate and is therefore not subject to inheritance tax.

However, this exemption depends on certain conditions:

- Premiums paid after age 70 are included in the estate and subject to tax, with a €30,500 allowance for all premiums paid.

- If you die before age 70, only the premiums paid in the last year of the contract are taxable, at a rate of 20%, after a €152,500 allowance. For amounts above €700,000, the rate is 31.25%.

Full tax exemption applies if the beneficiary is the deceased’s spouse or **PACS partner.

Med venlig hilsen / Kind regards

Cabinet Nicolas BRAHIN

Advokatfirma i NICE, Lawyers in NIC

Camilla Nissen MICHELIS

Assistante – Traductrice

1, Rue L

ouis Gassin – 06300 NICE (FRANCE)

Tel : +33 493 830 876 / Fax : +33 493 181 437

Camilla.nissen.michelis@brahin-avocats.com

Read more